P30 Monthly Return - Feature

P30 RETURNS

IMPORTANT NOTES

Reduced Frequency of Filing Tax Returns and Payments

Reductions in the filing and payment frequencies for VAT, PAYE/PRSI and RCT by smaller businesses are being extended to eligible customers from 1 January, 2014.

What are the benefits to eligible businesses?

The benefits are two-fold:

How will these changes be implemented?

Revenue will shortly write to each eligible business confirming that reduced frequency of tax returns and tax payments will apply from 1 January, 2014.

A copy of the letter will also be sent to the agent or tax practitioner on record for eligible customers (other than PAYE/PRSI customers).

Revenue will automatically extend the reduced filing and payment frequencies to eligible businesses without the need for any action on their part.

Reductions in the filing and payment frequencies for VAT, PAYE/PRSI and RCT by smaller businesses are being extended to eligible customers from 1 January, 2014.

- Businesses making total annual VAT payments of less than €3,000 are eligible to file VAT returns and make payments on a 6 monthly basis;

- Businesses making total annual VAT payments of between €3,000 and €14,400 are eligible to file VAT returns and make payments on a 4 monthly basis;

- Businesses making total annual PAYE/PRSI payments of up to €28,800 are eligible to make payments on a 3 monthly basis;

- Businesses making total annual RCT payments of up to €28,800 are eligible to file RCT returns and make payments on a 3 monthly basis.

What are the benefits to eligible businesses?

The benefits are two-fold:

- Improved cashflow by only having to make payments at the end of each 3, 4 or 6 monthly period, as appropriate.

- Reduced costs of administration through less frequent filing of tax returns

How will these changes be implemented?

Revenue will shortly write to each eligible business confirming that reduced frequency of tax returns and tax payments will apply from 1 January, 2014.

A copy of the letter will also be sent to the agent or tax practitioner on record for eligible customers (other than PAYE/PRSI customers).

Revenue will automatically extend the reduced filing and payment frequencies to eligible businesses without the need for any action on their part.

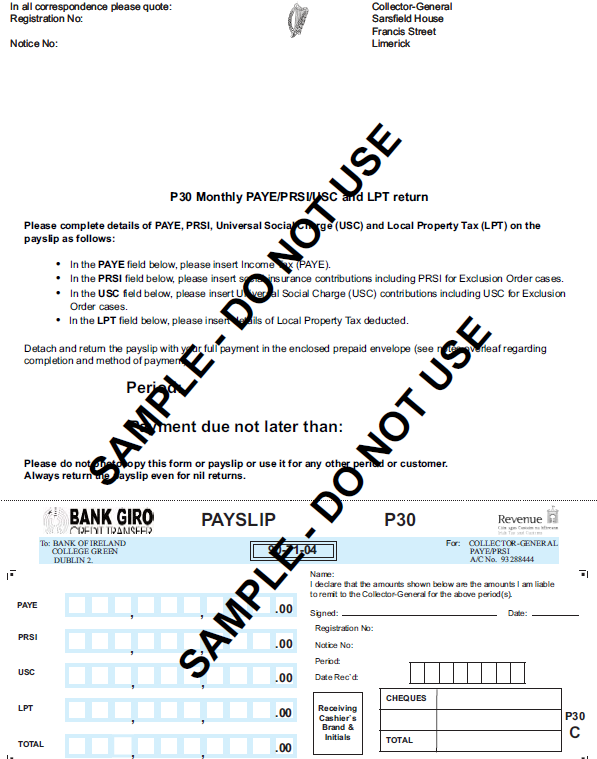

P30 RETURNS

Form P30 is a monthly or quarterly return of PAYE, USC, Parking Levy, Local Property Tax & PRSI to the Revenue Commissioners.

The P30 is the total of:

With effect from 1 January 2009, for employers who file their returns and associated tax payments via ROS, the existing time limits have been extended to the 23rd of the month immediately following the income tax month during which the deductions were made.

Where a return and associated payment are not made electronically by the new extended deadlines, the extended time limits will be disregarded so that, for example, any interest imposed for late payment will run from the former due dates and not the extended dates.

- the tax deducted from the pay (PAYE, USC, LPT) of all employees less any tax refunded to them

- the total PRSI contributions (the amount deducted from pay plus the amount payable by the employer)

With effect from 1 January 2009, for employers who file their returns and associated tax payments via ROS, the existing time limits have been extended to the 23rd of the month immediately following the income tax month during which the deductions were made.

Where a return and associated payment are not made electronically by the new extended deadlines, the extended time limits will be disregarded so that, for example, any interest imposed for late payment will run from the former due dates and not the extended dates.

With each payroll processed Thesaurus Payroll Manager builds the P30. To access this report go to Reports > P30 details>

- Click P30 by week number OR P30 by date

P30 by week

The P30 by week number calculates PAYE, USC, Local Property Tax, Parking Levy & PRSI liability up to the 5th of the following month. Monthly & Quarterly figures are shown.

P30 by date

The P30 by date calculates PAYE, USC, Local Property Tax, Parking Levy & PRSI liability up to the last date in the month. Monthly & Quarterly figures are shown.

Need help? Support is available at 01 8352074 or thesauruspayrollsupport@brightsg.com.

Glossary of TermsPayroll DeductionsGetting startedImporting from previous yearCompanyEmployeesPensionsBenefit in kindProcessing PayrollIllness BenefitMaternity BenefitReverse UpdateHolidaysP45Backup and RestoreReportsCSOP30Year endNotifying ROS of new employeesFeature Payroll

Introduction To FeatureDelete Feature PayrollSetting up EmployeesPayments FileDeductions FileDefault PaymentsDefault DeductionsPension SetupPension Related Deduction (PRD) or Pension LevyPeriodic InputIllness BenefitProcess PayrollFeature PayslipFeature ReportsP30 Monthly Return - FeatureP30 Quarterly Return - FeatureP30 Payment Records - FeatureP30 FOR ROS - Feature

LegalLeave EntitlementsSEPA Bank Payment Files