Employer Does Not Pay Sick Leave

If you do not know how much Illness Benefit the employee is receiving then you must make a best estimate and deduct PAYE from it in the week it is due to the employee. The below fields must be used in order to allocate the correct PAYE treatment to the Illness Benefit.

- No payment is made for the first six days of Illness or for any Sunday during the Ill period.

- The normal weekly rate of Illness benefit is €188.00, or €31.33 per day.

- Employees will receive the 6 day payment even if they normally work 5 days.

- Employer reduces the employees working hours to zero for the sick period.

- Employee claims and retains the DSP Illness Benefit of €188.00 per week

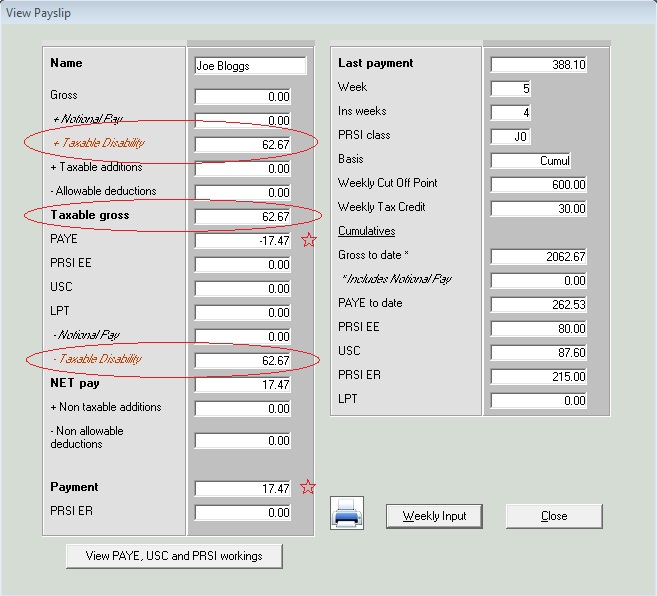

- Eventhough the employer is not paying the employee he must collect the tax on the Illness Benefit that the employee is receiving from DSP and record that he has taxed the Illness Benefit

PAYE 188.00 @ 20% €37.60

Less Tax Credit - €30.00

PAYE payable € 7.60

Employer does not make any payment to the employee.

Employer must collect €7.60 in PAYE due on the Illness Benefit received by the employee directly from DSP.

To tax the Illness Benefit in Thesaurus Payroll Manager

Payslips> Weekly/Monthly Input> Select the employee

Zeroise the employee hours or basic pay so that the employer reflects zero pay for the period.

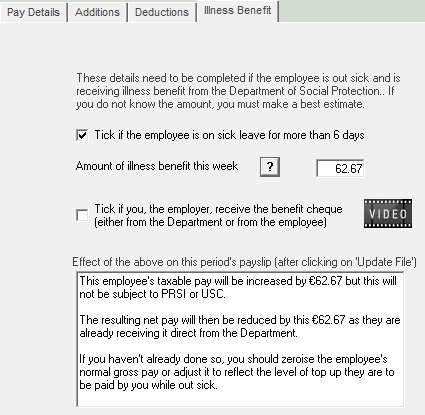

Select the Illness Benefit tab

Indicate that "... the employee is on sick leave for more than 6 days"

![]()

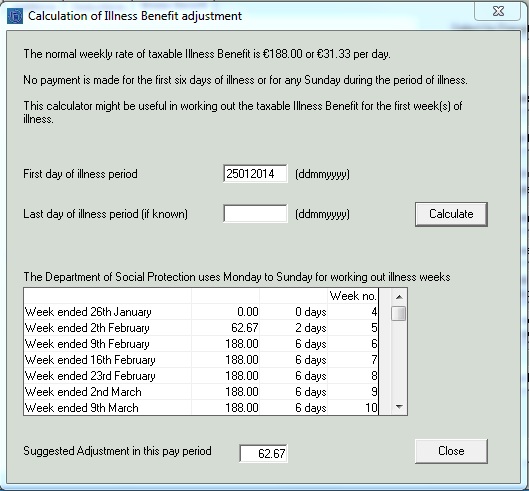

Illness Benefit Calculator

A built in Illness Benefit calculator will help you to calculate how much Illness Benefit the employee is eligible for in the pay period.

To access the calculator select the "?"

Enter the first date of sick leave (not the start date of Illness Benefit)

The calculator will predict the Illness Benefit that the employee is eligible for in this pay period and all future pay periods for as long as the sick leave continues.

The calculator will determine start dates from the date of the last pay period.

Enter the Illness Benefit

Enter the Illness Benefit for which the employee is eligible in this pay period.

You must collect PAYE on this amount.

Indicate that "... the employee is on sick leave for more than 6 days"

Enter the amount of Illness Benefit the employee is entitled to in this pay period (regardless of whether they have actually received it or not)

Click Update File

Employers must use the dedicated Illness Benefit feature in order to isolate the Illness Benefit figure from the employees normal pay as it must be declared to Revenue on all employee related Revenue returns;

P45

P35

P60

Need help? Support is available at 01 8352074 or thesauruspayrollsupport@brightsg.com.