Share Based Remuneration

Share Based Remuneration

2012 PRSI rules were amended to include the application of PRSI to Share Based Remuneration paid to employees, this continues in place since 2012.

Where an employee is in receipt of Share Based Remuneration it is subject to PRSI at a flat 4%, regardless of other earnings or unused PRSI-Free Allowance.

- Share Based Remuneration is subject to Employee PRSI only, it is not subject to Employer PRSI

- Share Based Remuneration should be included as income in determining the appropriate PRSI subclass to apply to the employees total income, but at all times ensuring that the total portion of Share Based Remuneration is subject to 4%

- Share Based Remuneration should NOT be included as income in determining the appropriate Employer PRSI subclass to apply and in charging Employer PRSI.

- In some cases this may result in a different subclass being applied to the employee and employer PRSI. If this is the case it is always the Employee's subclass that is recorded against the pay period and subsequently returned.

If you enter the phrase 'Directors fees' or 'Share based pay' in taxable additions, the software will split the PRSI calculation accordingly. If the Share based pay is awarded in shares, as opposed to income, then enter a non allowable deduction to the same value.

You may need to confirm this treatment with your accountant/tax advisor or if you are in any doubt to whether or not any portion of income is to be treated as share based remuneration.

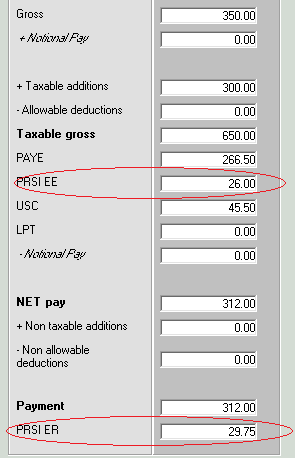

Calculating PRSI with Share Based Remuneration

Employee PRSI

Employees Weekly Salary €350.00

Share Based Remuneration €300.00

Total Income to determine Employee PRSI €650.00

Employee PRSI is deducted at subclass A1

Salary €350.00

€350.00 @ 4% = €14.00

Share Based Remuneration €300.00 at 4%

€300.00 @ 4% = €12.00

Total Employee PRSI deduction €26.00

Employer PRSI

Employer PRSI

Employees Weekly Salary €350.00

Share Based Remuneration €300.00 NOT SUBJECT TO EMPLOYER PRSI

Total Income to determine Employer PRSI €350.00

Employer PRSI is deducted at subclass A0 (i.e. at the rate of 8.50%)

Salary €350.00

€350.00 @ 8.50% = €29.75

Total Employer PRSI deduction €29.75

Revenue / Department of Social Protection submissions will all reflect PRSI contributions for the period at the Class of A1

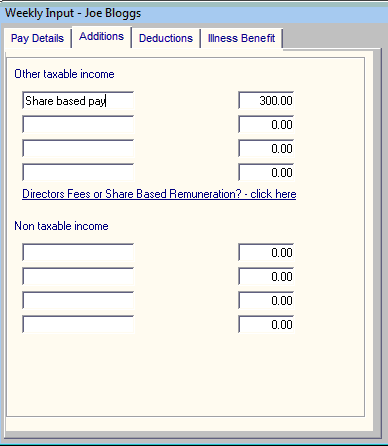

Setting up Share Based Remuneration in Thesaurus Payroll Manager

Go to Employees> Add/Amend Employees>

Select "Additions"

Alternatively go to Payroll> Weekly/Fortnightly/Monthly Input>

Select "Additions"

Within the first "Other Taxable Income" the narrative must be entered as "Share based pay" in order to allocate this field to Share Based Remuneration and to apply the correct PRSI treatment to any amount entered.

Once you start to enter "Share based pay" the field will auto fill.

The PRSI will be deducted accordingly

Need help? Support is available at 01 8352074 or thesauruspayrollsupport@brightsg.com.

General

Help2016 Budget - Employer SummaryOrdering for next yearPayroll UpgradesPayroll CalendarCalculatorImport Hours from Text or CSV FileFull periodic CSV ImportPension Related Deduction (PRD) or Pension LevyComputational AnomalyDirectors FeesShare Based RemunerationSpecify end dates for additions or deductionsExporting payroll journals to accounts softwareGift Cards - Integration and tracking

Glossary of TermsPayroll DeductionsGetting startedImporting from previous yearCompanyAdd/ Amend EmployeesNotifying ROS of new employeesProcessing PayrollBank FilesReportsP30sProcessing LeaversBenefit in KindIllness BenefitMaternity BenefitPaternity BenefitPensionsReversing the PayrollBackup and RestoreYear endCSOHolidaysLeave EntitlementsLegalFeature PayrollTransferring Payroll Manager from one PC to another