USC Exempt Status v USC Exempt Income

USC Exempt v USC Exempt Income

Employers should be wary of the difference between USC exempt status (as per P2C/tax credit certificate) and employees in receipt of USC exempt income.

If an employee expects their income to be less than €13,000 in the tax year they can contact Revenue to make a declaration of same, it is only the employee themselves that can make this declaration. Revenue will update the employees USC status to USC exempt and issue a new P2C/tax credit to the employer. The employer will follow this instruction and USC will not be deducted from the employee accordingly.

If an employee is in receipt of USC exempt income, e.g. Community Employment Participants, Department of Social Protection payments, these employees will not necessarily hold USC exempt status on the P2C/tax credit certificate. The exempt income itself should be flagged as USC exempt within the payroll.

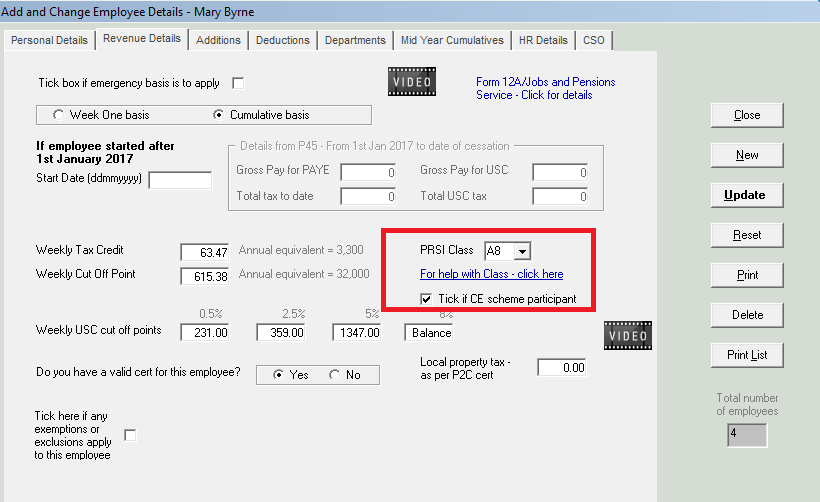

Community Employment Participants are allocated PRSI class A8 or A9. Once A8 or A9 is assigned to the employees record in Revenue Details the user will have the option to indicate that the employees income is USC exempt. Simply tick the dedicated field Tick if CE scheme participant, as shown below.

Need help? Support is available at 01 8352074 or thesauruspayrollsupport@brightsg.com.

GeneralGlossary of TermsPayroll Deductions

Universal Social Charge (USC)Universal Social Charge (USC) - CalculationsUSC Exempt Status v USC Exempt IncomePAYEPRSILocal Property Tax (LPT)Bike to Work SchemePension Related Deduction (PRD) or Pension Levy

Getting startedImporting from previous yearCompanyAdd/ Amend EmployeesNotifying ROS of new employeesProcessing PayrollBank FilesReportsP30sProcessing LeaversBenefit in KindIllness BenefitMaternity BenefitPaternity BenefitPensionsReversing the PayrollBackup and RestoreYear endCSOHolidaysLeave EntitlementsLegalTransferring Payroll Manager from one PC to anotherThesaurus ConnectGDPR