TWSS - Transitional Phase (effective until 4th May 2020)

PLEASE NOTE THIS SCHEME HAS NOW ENDED.

The Government has announced a more enhanced scheme for employers and employees who are facing difficulties as a result of the COVID-19 outbreak.

This new scheme is called the 'Temporary Covid-19 Wage Subsidy Scheme' and takes effect from Thursday 26th March 2020.

This replaces the previous Employer Covid-19 Refund Scheme.

Comprehensive Revenue guidance on the Temporary Covid-19 Wage Subsidy Scheme can be found here

We have summarised the key points of the Scheme below.

General Points

- This scheme replaces the Employer Covid-19 Refund Scheme from 26th March 2020.

- The scheme applies to employers who may wish to top up employee payments and those who are not in a position to do so.

- Employers already registered for the Covid-19 Refund Scheme do not need to re-register for the new scheme.

- Employers that are not registered but wish to register for this scheme can do so through myEnquiries (details on how to do this are in the Revenue link above).

- The Scheme is due to run until the end of August 2020.

Who qualifies for the scheme?

To qualify, employers:

- must be experiencing significant negative economic disruption due to Covid-19

- must be able to demonstrate, to the satisfaction of Revenue, a minimum of a 25% decline in turnover

- be unable to pay normal wages and normal outgoings fully

- retain their employees on the payroll.

The Scheme is restricted to employees who were on the employer’s payroll as at 29 February 2020, and for whom a payroll submission has already been made to Revenue in the period from 1 February 2020 and 15 March 2020

Where employers didn't fulfil their PAYE reporting obligations for February 2020 by 15 March 2020, please click here for further information.

See Revenue guidance on employer eligibility and supporting proofs here

Phase 1 of the Scheme

The scheme is to be run in two phases:

- Under Phase 1, employers can pay 70% of the employee’s average weekly net pay as a non-taxable payment (net pay = Gross less Income Tax, USC & Employee PRSI) and in turn receive a refund from Revenue for this.

This payment is capped at: - €410 per week where the average net weekly pay is less than or equal to €586

- €350 where the average net weekly pay is greater than €586 and less than or equal to €960

(employees with an average net weekly pay greater than €960 will be excluded from the subsidy scheme - please refer to 'Employees whose average weekly pay is higher than €960' below for recent changes)

- The period for calculating an employee's average weekly pay is January & February 2020 (an average pay calculator is provided in Thesaurus Payroll Manager)

- The refund from Revenue will, in general, be made to the employer within 2 working days after receipt of the payroll submission (PSR)

- During Phase 1, employers must work out the payment that can be made to the employees i.e. the 70% tax free payment and the maximum top-up allowed (an average pay calculator is provided in Thesaurus Payroll Manager)

- Revenue will automatically refund €410 per week per employee on the scheme (as they won’t know what employees are entitled to)

- At a later date, Revenue will perform a reconciliation and will look for repayment of any overpayments

Phase 1 - Top Up Payments

- Employers may top up this payment if they are in a position to do so.

- This top up amount, when added to the employee’s subsidy payment, cannot be greater than the employee's average net weekly pay.

- If an employer tops up payments by more than the permitted amount, their subsidy will be tapered i.e. for every €1 extra paid to an employee, they will lose €1 on the subsidy

- Any top-up payment made is taxable and USC-able

- The combined payment is to be processed under PRSI Class J9

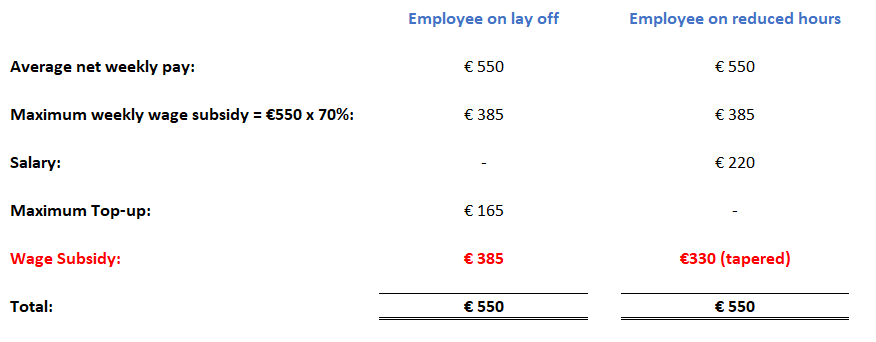

- The maximum additional pay/top-up is the same for all employees - that is, the treatment is exactly the same for employees on short-time or reduced hours/pay.

Where an employee is on reduced hours, care must be taken that their salary along with their subsidy payment does not exceed their average net weekly pay. Where the maximum allowed is exceeded, the subsidy must be reduced accordingly.

Example:

Please note: where the subsidy is to be reduced, this must be done manually by the user in Thesaurus Payroll Manager.

Phase 2 of the Scheme

Phase 2 of the Wage Subsidy Scheme has been announced to take effect from 4th May.

We are currently in a consultation phase with Revenue and will provide more information on how phase 2 will operate in due course.

In the meantime, general information regarding Phase 2 can be accessed here

Phase 1 - Processing the Payment in Thesaurus Payroll Manager

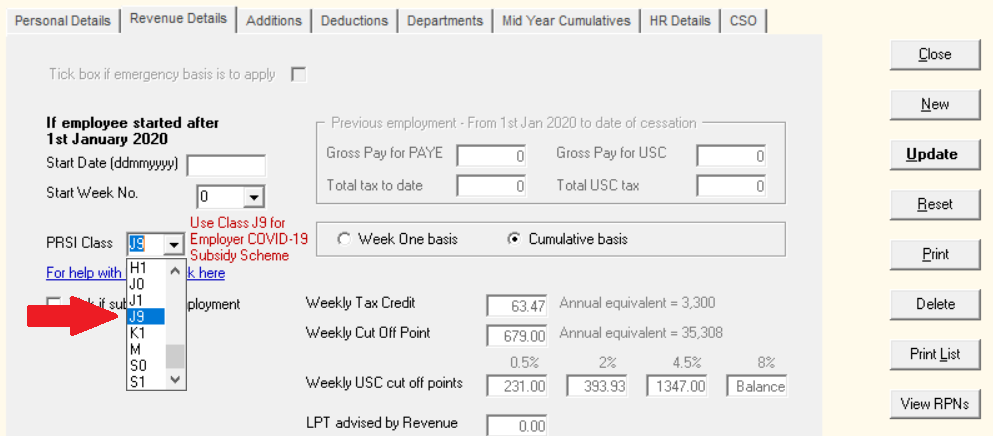

In order for Revenue to recognise employees being paid under the scheme, they have requested that PRSI Class J9 is used.

a) Within the employee's record, select PRSI class J9 within their Revenue Details utility.

An information page will appear for you to read - click 'OK' to proceed, followed by 'Update'.

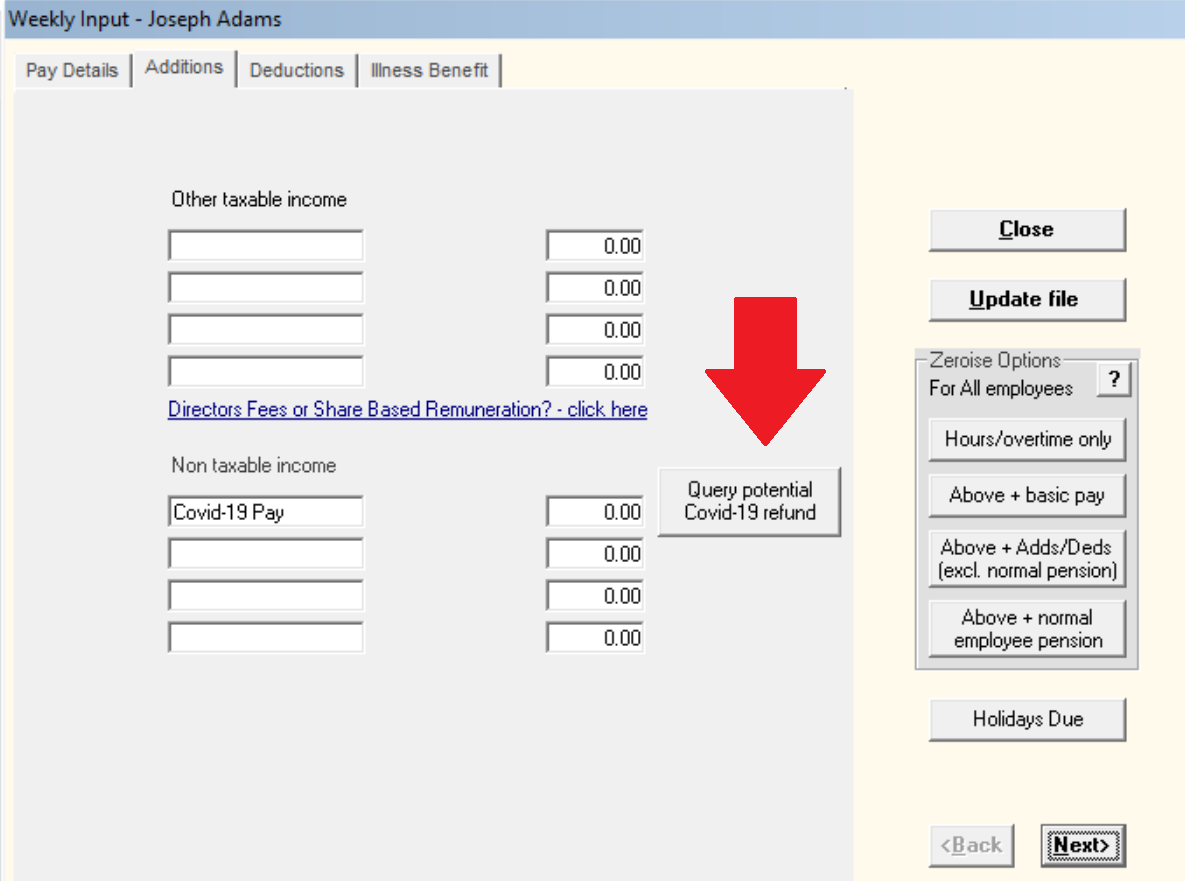

b) Now access Weekly/Monthly/Fortnightly Input and select the employee.

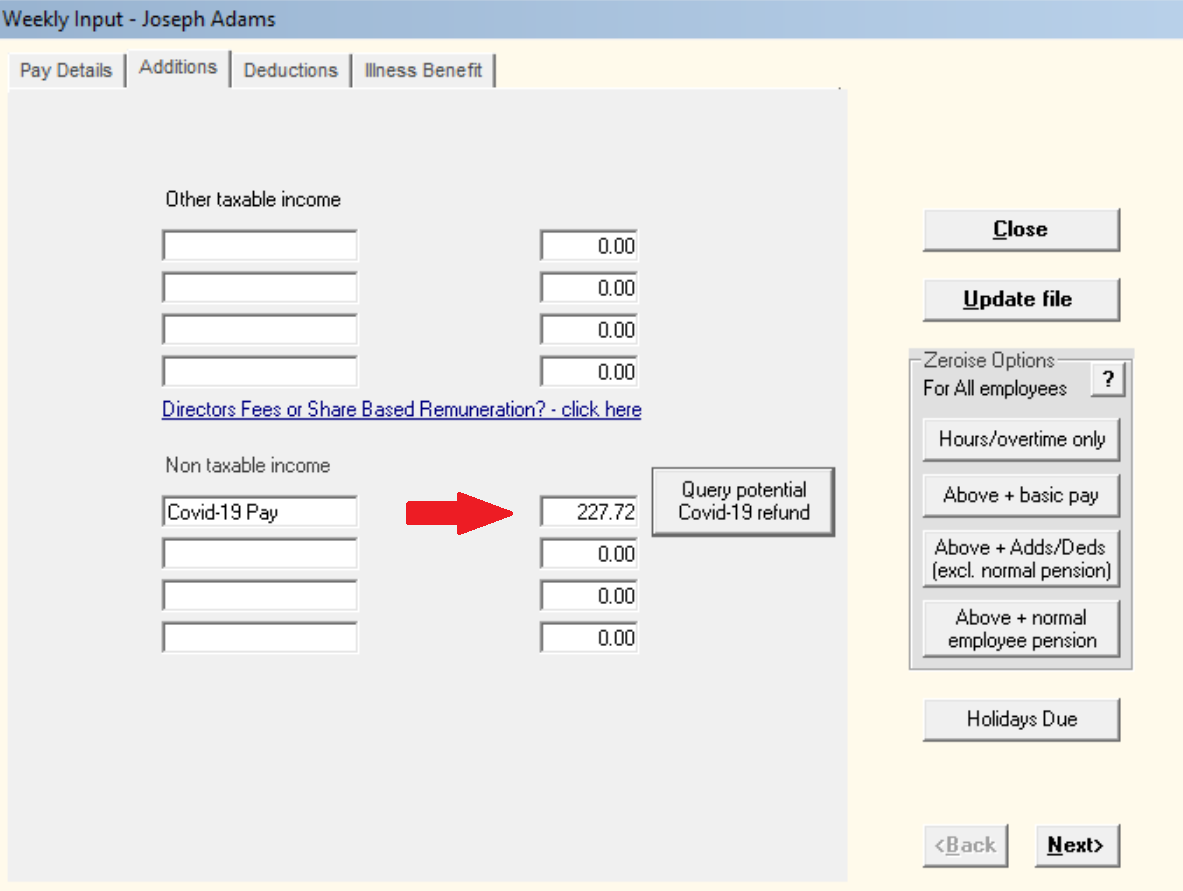

c) Click into their Additions utility.

- If you already know the refundable 70% payment amount to pay to the employee, enter this in the Covid-19 Pay amount box.

- Should you wish Thesaurus Payroll Manager to assist you in calculating the refundable 70% payment amount, click 'Query potential Covid-19 refund':

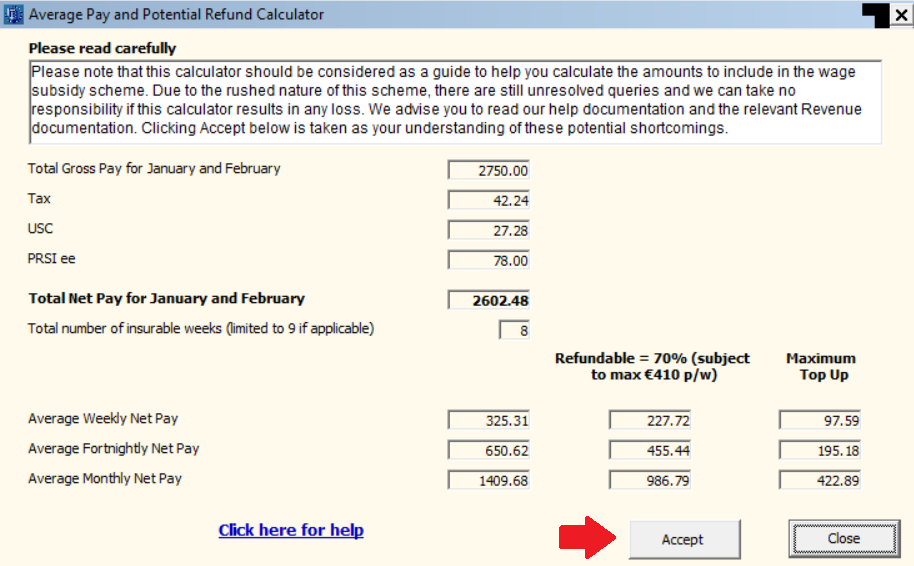

d) The calculator will now ascertain what the refundable payment amount is, based on the employee's average periodic net pay during January and February (and taking into account the capped payment thresholds).

Should you be in a position to be able to top up this payment, the calculator will also calculate the maximum top up amount you can give without affecting your subsidy.

Important notes regarding the calculator

- This calculator should be considered as a guide to help you calculate the amounts to include in the wage subsidy scheme. Due to the rushed nature of this scheme, there are still unresolved queries outside of our control and which we still await clarity on. We can therefore take no responsibility if this calculator results in any loss. We advise you to consult relevant Revenue guidance. Clicking 'Accept' will be taken as your understanding of these potential shortcomings.

- It should also be noted that should you decide to pay a top-up amount above what the calculator recommends, this could result in the tapering of the refund or no refund at all.

- Where an employee is on reduced hours but still receiving some salary, we ask you to refer to the 'Top Up Payments' section above in case a manual adjustment to the subsidy amount is required by the user.

e) Click Accept to proceed.

f) Read the prompt and click OK

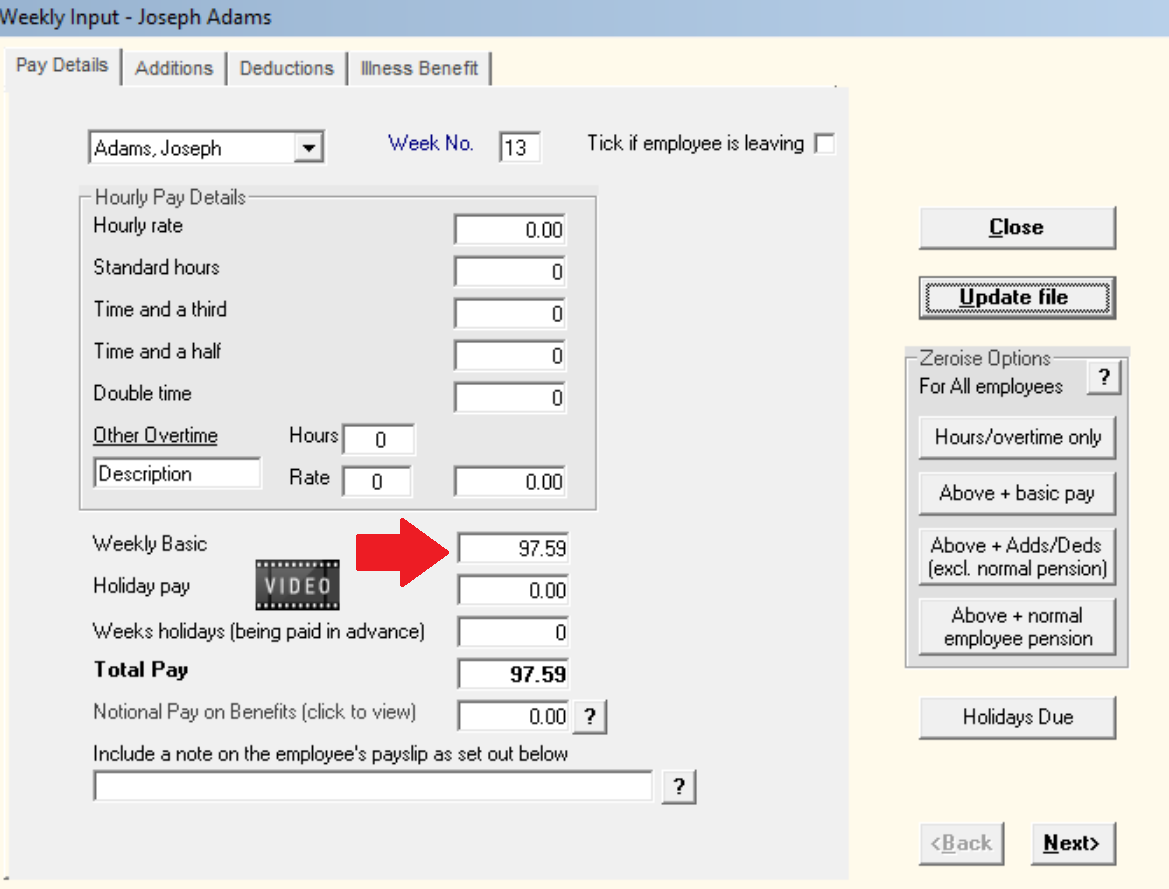

The Periodic Input screen will now populate with the applicable non-taxable pay amount and it will also populate the employee's basic pay with the amount of the maximum top up:

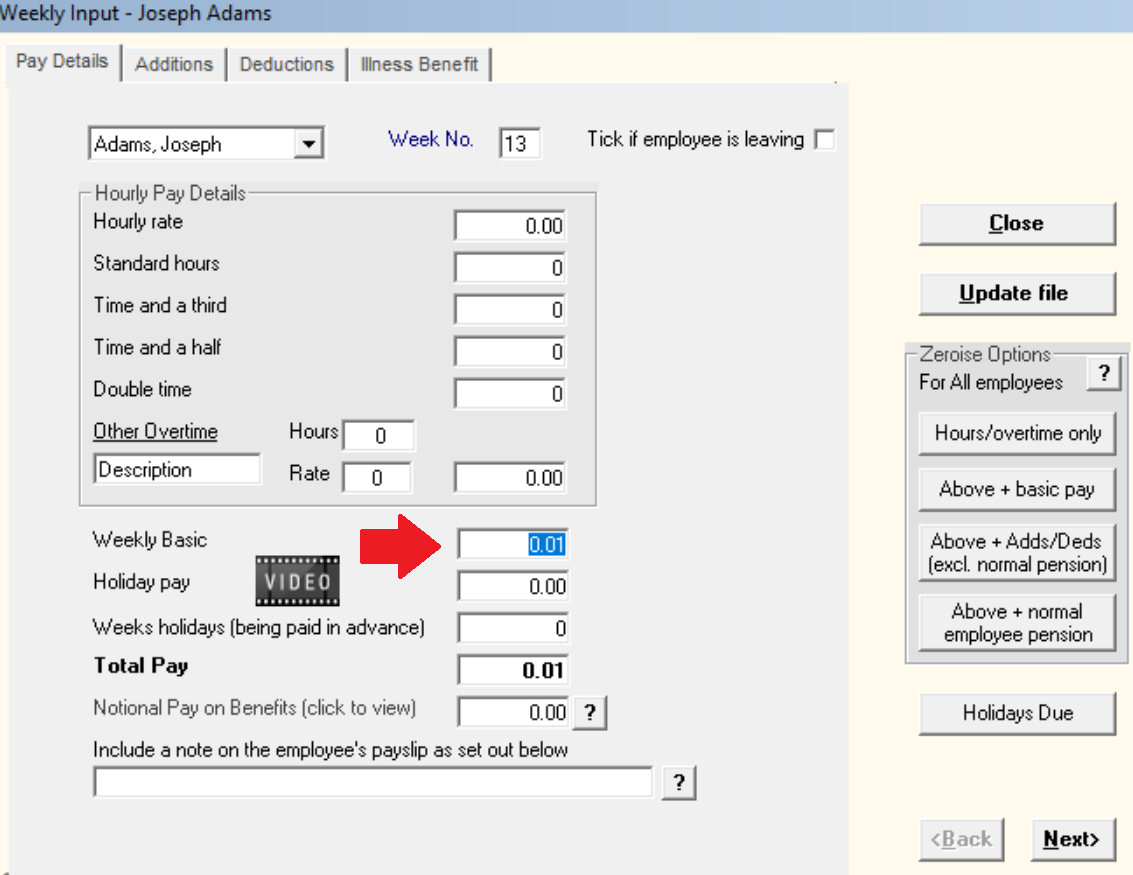

g) If you don't wish to make a top up payment, it is important to change the basic pay amount to €0.01 - this will act as a notional gross pay amount in order to generate a payroll submission:

Please note: All other payments, benefits and deductions will be zero-ised.

h) Click 'Update File' to save your changes and repeat the process for further employees, if required.

On updating your payslips, the above will now flow through to the payroll submission (PSR) for submission to Revenue.

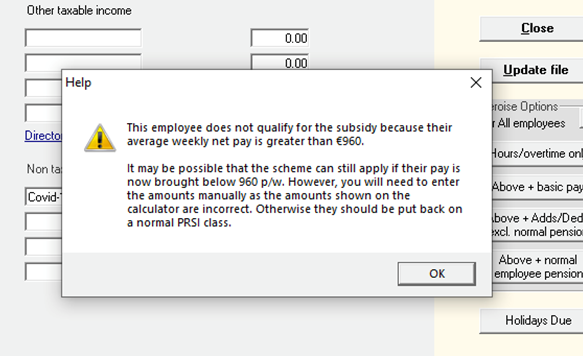

Employees whose average weekly pay is higher than €960

Where it is ascertained that an employee's average net pay for January and February exceeds €960 per week, it will be brought to your attention that the employee does not qualify for the subsidy when you query the potential Covid-19 refund:

Please note: From 16th April 2020, the wage subsidy is available to support employees where their average weekly net pay was greater than €960. In order to avail of the scheme, the employee's earnings must be reduced.

Where the employees earnings have now been reduced by:

- More than 20%, a subsidy of up to €205 would be payable

- More than 40%, a subsidy of up to €350 would be payable

For example:

- employee has an average weekly net pay of €1,250

- employee's earnings now reduced to €750 (40% reduction)

- Subsidy due €350

To enter the subsidy for these employees, please close the calculator and enter the subsidy payment and gross pay manually.

Using the example above, the gross pay should be entered as €610 and the wage subsidy figure should be entered as €350. The combined pay cannot exceed €960.

Please note: if the employee isn't eligible because the earnings don't qualify, please change the employee's PRSI class back to their regular PRSI class e.g. PRSI class A1.

Tax/USC Refunds

In many cases the payment of the Temporary Wage Subsidy and any additional income paid by the employer will result in a tax/USC refund to the employee. Any tax and USC refunds that arise can be repaid by the employer and Revenue will also refund this amount to the employer.

**In this instance, the Tax Details Report within Thesaurus Payroll Manager will not match the Revenue statement. In this case, the Revenue Statement will be correct as Revenue will account for the refunds.

Re-hiring Staff

- Employees who have been ceased as a result of the Covid crisis can be re-hired and paid under the subsidy scheme. In this instance, the DEASP claim should be ceased

- However employees must have been included in submissions between 1st February 2020 and 15th March 2020 under the same PPSN to qualify.

- Please note: the software will not calculate average earnings in this instance, so a manual calculation will be required.

Employees claiming from the DEASP directly

Employers must not operate this scheme for any employee who is making a claim for duplicate support (e.g. Pandemic Unemployment Payment) from the DEASP. Where an employee previously laid off has been re-hired, the employee will qualify for the Subsidy scheme if their DEASP claim is ceased (see above).

Need help? Support is available at 01 8352074 or thesauruspayrollsupport@brightsg.com.