RCT and VAT - schools

RCT - click here for detailed guidance

VAT - click here for detailed guidance

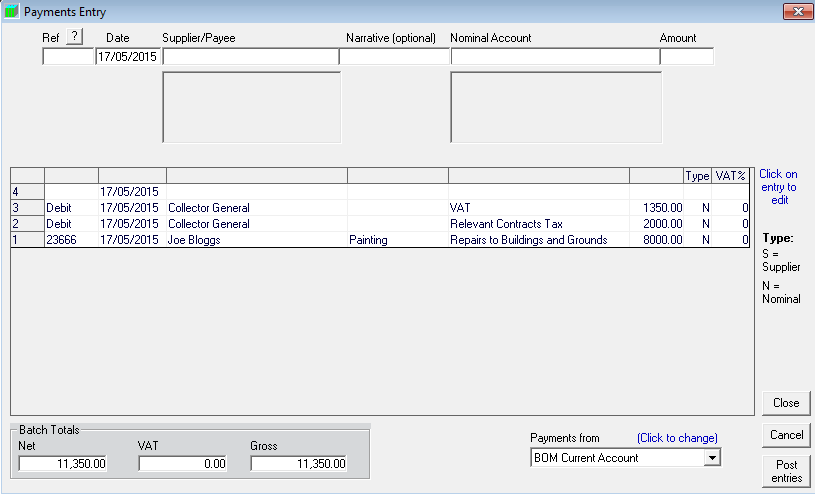

Posting when making a payment to the subcontractor e.g.

a. Mr Joe Bloggs paints the school for €10,000 excluding

VAT and gives an invoice to the school.

b. Reverse Vat @13.5% = €10000*13.5%= €1,350

c. RCT @ 20% = €10000 * 20% =€2000

Click on the image below to zoom.

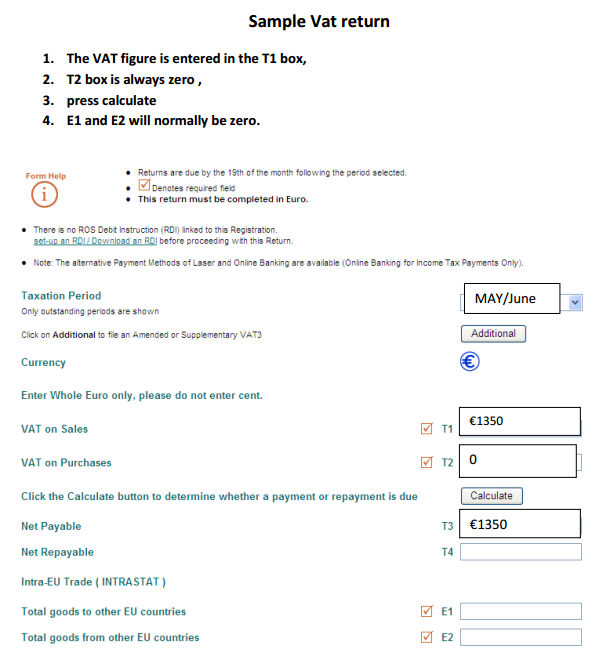

Although the above demonstrates all parts of the transaction, the reality is that the VAT and RCT amounts will be paid on different dates to the date that payment was made to the subcontractor.

The Vat payment of €1,350 will be returned on the May/June VAT return and the payment should be made using ROS and it is due by the 23rd July.

The RCT payment of €2,000 will be returned on the June RCT return and the payment should be made using ROS and it is due by the 23rd June.

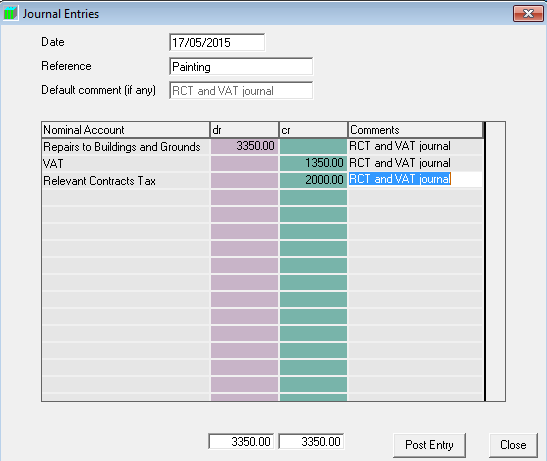

A journal would then be required from the VAT and Relevant Contracts Tax nominal accounts to reflect the fact that these costs are a part of the overall cost of painting (as follows)

Need help? Support is available at 01 8352074 or thesauruspayrollsupport@brightsg.com.